Despite fears that Europe may face a gas crunch following the cancellation of Nord Stream 2, analysts at Wood Mackenzie say Europe is currently in a better situation than it was at the start of the 2021/22 winter.

Kateryna Filippenko, principal analyst, Europe gas research, said: “Mild weather and increased liquefied natural gas (LNG) supplies have softened the impact of continuously low Russian flows and resulted in higher volumes of gas in storage.

“From record lows at the start of winter, storage levels have now re-entered their five-year range, albeit on the lower side, and are on track to be in a more comfortable position by the end of March.”

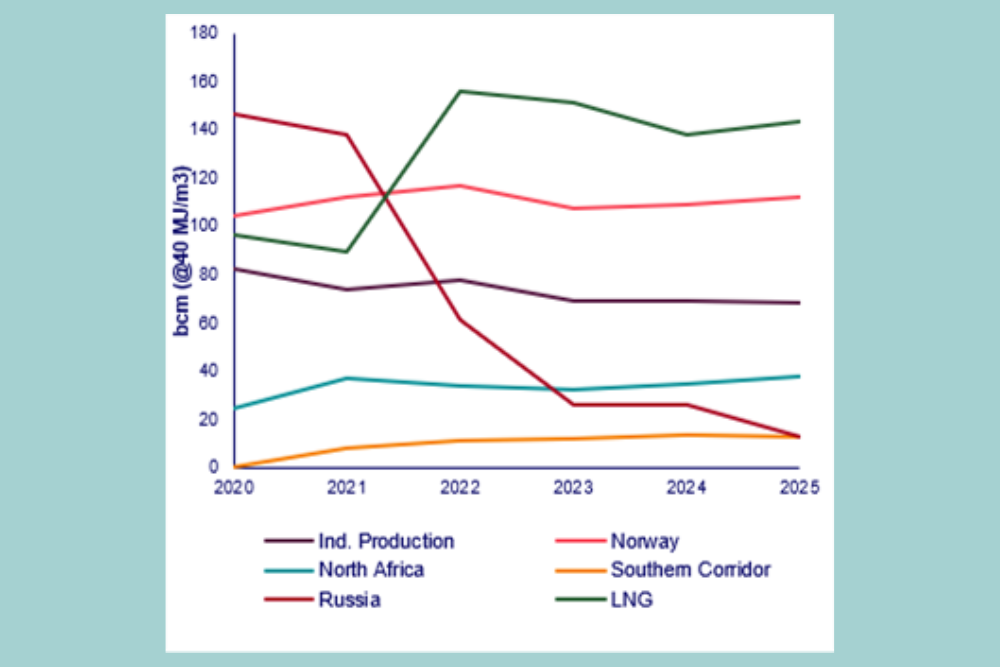

She said that Wood Mackenzie’s analysis shows that in January-February this year, there was more LNG in Europe’s gas system than Russian gas. High European prices have helped, but this is mainly a result of Asia starting the year with high inventory levels, coupled with mild local temperatures which freed up some LNG cargoes for Europe.

High prices, which are likely to remain through 2022, will encourage Norway to continue strong exports into Europe and will attract more LNG cargoes into Europe, Filippenko said. High hydro levels in Brazil will free up additional LNG cargoes for Europe.

“This will reduce the requirement of Russian gas through 2022. Even relatively low flows at current contractual levels – with Poland and Ukraine transit routes running below full capacity – will result in a comfortable storage position ahead of the next winter,” she added.

“We expect levels to reach about 85 per cent by the end of October, in contrast to 74 per cent at the start of the current winter.

“Overall, the current supply and storage situation means Europe is in a better position both to navigate 2022 without Nord Stream 2 and to prepare for the next winter.”

However, 2023 will be more challenging. Continuous decline of indigenous production coupled with lower availability of LNG supply for Europe – a result of limited supply coming online coupled with increasing Asian demand – will tighten the market further.

Filippenko said Europe may struggle to refill its storage to a comfortable level through summer 2023 and prepare for winter.

She said: “Under average weather conditions, Russian flows limited to contracted levels would result in storage levels at 75 per cent ahead of the winter 2023/24 – similar to levels ahead of the 2021/22 winter.

“If no additional gas is made available from Russia, Europe would be exposed to weather dynamics throughout next winter, similarly to this winter, with prices remaining high and volatile. Only through increased flows from Russia the situation could ease – this is via existing spare capacity on transit routes through Ukraine and Poland – ensuring higher availability through winter 2023/24.”

Despite improved market dynamics, there is further upside risk to current prices in 2022, as traders price in the risk of Russian supply disruption. An expected price reduction in 2023, as the current forward curve suggests, may not eventuate if Russian imports are limited to contracted levels.

Filippenko said: “If Russian exports to Europe are disrupted, things could obviously get a lot worse. Europe may be able to cope if supply disruptions are limited to Ukraine transit. It would have to pull every lever in the energy system to keep the lights on – reducing gas burn and cranking up mothballed nuclear and coal plants; maximising indigenous gas production and pipeline imports; persuading Asian buyers to use coal and free up LNG.

“But this would only be a temporary solution to get through the summer and would leave Europe with perilously low storage volumes going into winter 2022/23 and risks demand disruptions. Winter prices next year could be higher than 2021/22.”

She added: “If all Russian gas is cut off, Europe would have no chance of coping. Were all gas flows to stop today, Europe could well muddle through in the short term, given higher storage inventories and low summer demand.

“But in the event of prolonged disruption, gas inventory couldn’t be rebuilt through the summer. We’d be facing a catastrophic situation of gas storage being close to zero for next winter. Prices would be sky high. Industries would need to shut down. Inflation would spiral. The European energy crisis could very well trigger a global recession.”