Global oil markets are facing a period of uncertainty as multiple factors converge to influence crude prices and supply dynamics.

Brent futures are hovering near US$73 per barrel as traders weigh geopolitical risks against oversupply concerns and shifting production patterns in North America.

Israel’s restrained retaliation against Iran last weekend initially cast a bearish shadow over the market, easing fears of a wider Middle East conflict that could disrupt oil supplies.

However, ongoing tensions in the region continue to inject volatility into crude prices.

Meanwhile, China’s economic outlook remains a key focus for oil demand projections. Recent manufacturing data showed signs of improvement, with the PMI rising to 50.1 in October — its first growth in six months.

Yet challenges persist, including weak producer prices and sluggish external demand, as policymakers aim to sustain momentum towards a 5 per cent growth target.

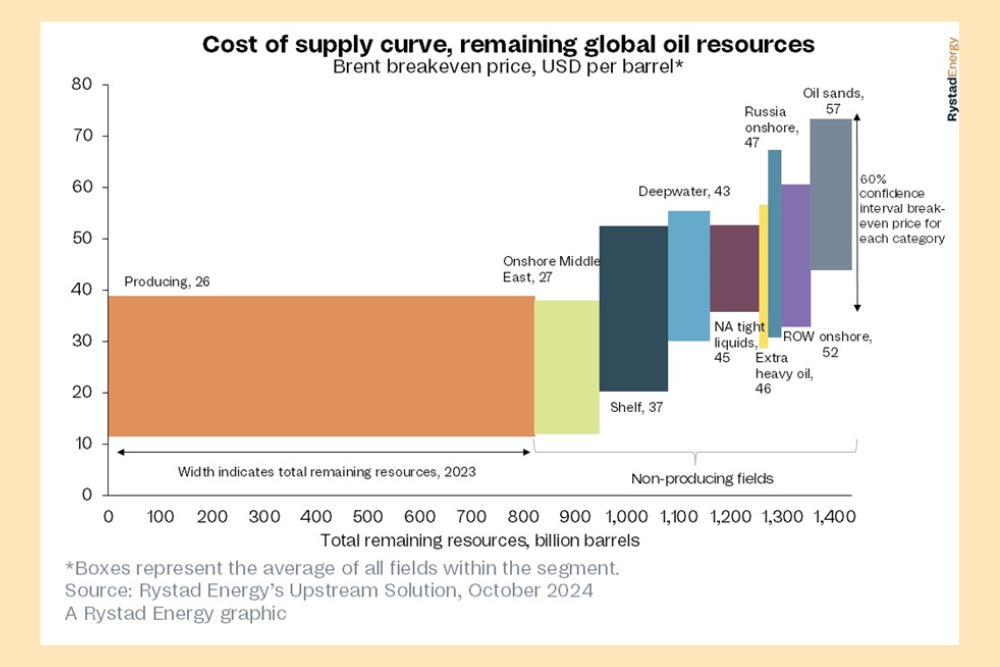

In North America, crude production is on an upward trajectory. Rystad Energy has upgraded its U.S. oil production forecast for Q4 2024 by about 150,000 barrels per day (bpd), citing more efficient completion activity.

The firm projects total U.S. crude output to reach 13.5 million bpd by December 2024 and 14.4 million bpd by the end of 2026.

Canada is also seeing significant growth in crude exports, particularly to Asian markets.

The Trans Mountain pipeline expansion, which began operations earlier this year, has increased export capacity by 590,000 bpd.

As a result, Canadian crude oil exports via Trans Mountain jumped to an average of 656,000 bpd in Q3 2024, a 53 per cent increase from Q2.

Two-thirds of this oil is now being sent to China, India, South Korea, and Japan.

The OPEC+ alliance is closely monitoring these North American production trends as it considers its next moves.

There are indications that the group may delay unwinding its production cuts scheduled for December, which could provide some price support.

Adding to the market’s complexity is the upcoming U.S. presidential election on November 5.

The outcome could have significant implications for global trade relations and energy policies, potentially affecting oil supply fundamentals.

Mukesh Sahdev, Global Head of Commodity Markets – Oil at Rystad Energy, summarised the current market sentiment, stating: “Oil markets are anxious this week, with the US elections on the horizon and China’s economic fortunes taking a rare positive turn despite tariff headwinds ahead.

“News of crude stock draws and a potential delay of OPEC+ cut unwinding for December is adding some support as Brent futures inch close to US$73 per barrel.”

As these various factors unfold, oil market participants will be closely watching for any shifts in supply-demand dynamics that could impact crude prices in the coming weeks and months.