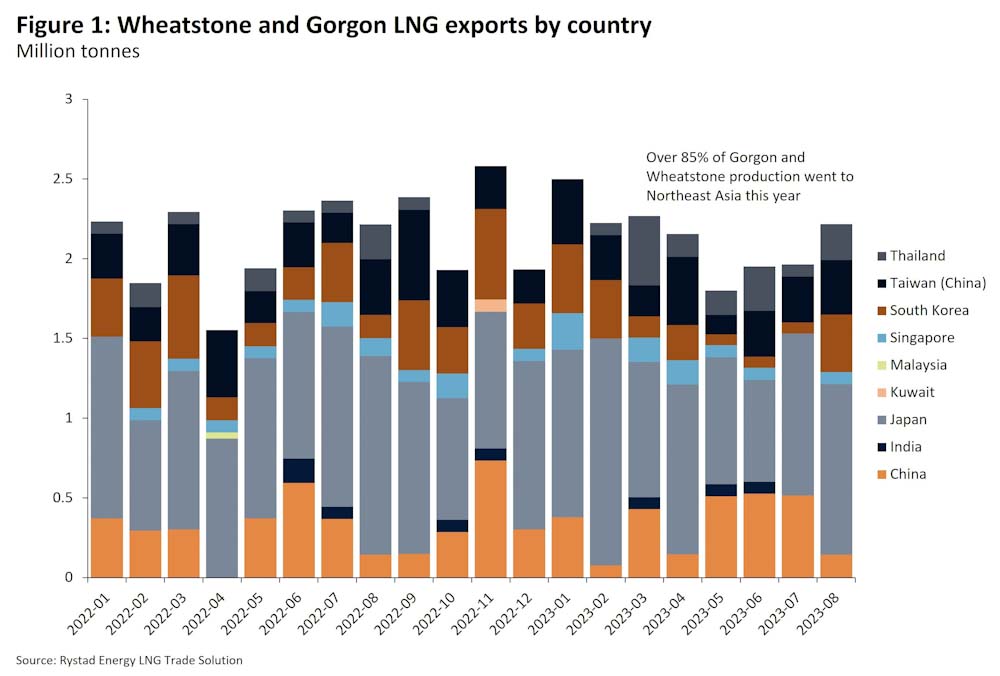

Volatility has returned to gas markets as workers at Chevron’s Wheatstone platform and LNG facility, as well as the Gorgon LNG facility in Australia, went on strike on 8 September after the five-day negotiations with the US supermajor failed.

The front-month Title Transfer Facility (TTF) opened at over $12 per million British thermal units (MMBtu) on 8 September, which is 25 per cent lower than the recent high on 22 August, when concerns over the impact of the strike were only pervasive.

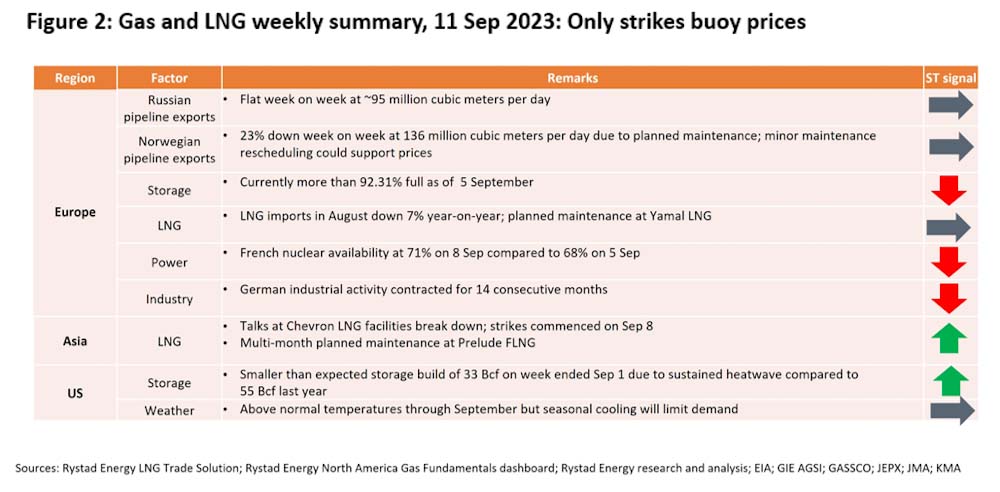

However, according to an analysis by Rystad Energy, the potential impact of the strikes is likely the only bullish element in the near-term market, given the entry into the pre-winter shoulder season and other indicators are bearish in both Europe and Asia.

A complete shutdown of production at Gorgon and Wheatstone would impact around 6 per cent of global production but this remains a tail risk noted to Rystad Energy, given the precedent already established at the neighboring Northwest Shelf.

“Given the importance of these facilities for Northeast Asian buyers – more than 68 per cent of capacity is contracted to Northeast Asian buyers (with actual exports to Northeast Asia over 80 per cent) – we anticipate Chevron is under pressure to accelerate resolution,” Rystad said in its analysis.

Image courtesy Rystad Energy

The countries where winter demand could surge (and price insensitive) are very comfortable this year.

European storage is now over 92 per cent full, while South Korea and Japan have additional nuclear capacity available this winter year-on-year.

As such, an increase in prices is more likely than not to simply see demand from the more price-sensitive countries recede.

Recent economic data from Germany also paints a bearish picture for the rest of the year.

As of July, German industrial production remains 7 per cent below pre-Covid levels, and production in energy intensive sectors is 11 per cent down on the year.

The economic outlook has worsened since GDP data for the second quarter implied a stagnating, rather than a contracting economy.

Industrial gas consumption is likely to be wary of the current unstable equilibrium in the gas market and, as such, a material recovery can only be expected once a period of sustained calm is achieved – the $2.7 per Metric Million British thermal unit spread on the forward curve between November-delivery and January-delivery is not helping.

Image courtesy Rystad Energy