The costs associated with onshore pipeline projects are likely to increase by between 4 and 6 per cent globally by the end of 2022 against current levels, new Rystad Energy analysis reveals, as prices continue to surge for labour, raw materials and transportation.

Materials in particular – which account for 30-40 per cent of the total cost for a pipeline – are expected to become 2-3 per cent more expensive in the same period and may approach $1 million per kilometre in leading pipeline regions such as the US.

A recent increase in steel demand has also led to higher iron ore prices, thus pushing up steel costs. Moving forward, the removal of tax rebates for line pipe in major export hubs like China could result in higher material costs, hence making Chinese exports more expensive.

In addition, prices for other pipeline construction materials – such as valves and flanges – have also spiked. The price index for pipeline flanges and valves in the US, for instance, has increased by more than 30 per cent since early 2020.

Rystad Energy notes that the anticipated rise in material costs will not be driven by an increase in general steel prices – as they are expected to slide next year – but instead by the present regulatory hurdles and a lull in pipeline development activity.

This, in turn, could hinder operators from locking in long term agreements with steel suppliers as prices take a turn for the better.

Additionally, stronger than expected demand from other industries, combined with the slow pace of pipeline project sanctioning activity, could push pipeline operators to the back of the queue to secure large orders, thereby forcing them to pay a premium to procure the required quantities.

Sumit Yadav, analyst in Rystad Energy’s energy service team, said high steel prices and rapidly growing wages for key pipeline trades could emerge as significant challenges for operators looking to drive costs down.

“When also factoring in higher transportation costs – led by a strong rebound in crude prices – the total price tag of pipeline projects is set to test operators,” Yadav said.

Construction and installation costs are the largest cost components of a pipeline project, potentially accounting for nearly half the total cost. Compared to other cost elements, which may undergo periods of decline, construction and installation costs have been highly resilient, driven in large part by rising wages, which can account for more than 50 per cent of these costs.

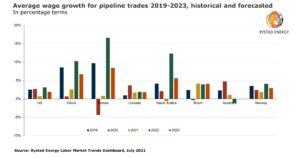

Rystad Energy provides the example that wages for major pipeline construction trades such as welders, construction equipment operators, electricians, plumbers, construction managers and drivers – have not dropped in the US despite a COVID-19 induced downturn and are expected to increase by more than 5 per cent by the end of 2023 compared to current levels.

Based on the company’s Labor Market Trends Dashboard, Rystad expects wages for major pipeline trades to grow at an average of about 8 per cent across major pipeline regions by the end of 2022 against current levels. This means an expected rise of 2 to 3 per cent in construction and installation costs during this period.

The cost pressure exerted by rising wages could further intensify as the US construction industry still lacks more than 200,000 workers, according to the US Department of Labor.

Rystad Energy’s notes that while the difference in wage growth across the various regions may allude to direct cost savings, this is partly offset by differences in productivity.

For instance, while wages in Asia can be around 80 per cent lower than US wages for pipeline trades, labour productivity in the US is also about three to four times higher. This reduces the benefits offered by the lower wages in Asia.

Right-of-way costs have historically been largely limited to nearly 5 per cent of total project costs across most regions. However, given the boom in renewable energy projects and a notable shift in government sentiment, especially in regions like North America, it would hardly be surprising to see these costs also escalate in the coming years.

For instance, Rystad Energy’s Onshore Pipeline Cost Estimating Dashboard suggests rock clearing costs can more than quadruple for a pipeline stretch covered by solid rock instead of common rock. Similarly, a pipeline passing through a semi-urban setting instead of a rural setting could be around 30 per cent more expensive.